Introduction to the foreigners

Many of the Double O games have a concept of “foreigners” who buy trains at the end of sets of Operating Rounds. This not only keeps the trains moving in the presence of timid train buyers, but makes the distribution of available trains in a given game uncertain. I borrowed this idea in 1843, extending it so that the foreigners would not just buy a train at the end of every set of Operating Rounds, but if they bought the last train of a rank they would also buy the first train of the next rank as well, thus lurching the game forward and shortening the train distribution and speeding the train rush even more.

Extending the system

1843’s extension worked well, accomplishing most of what I expected in

providing an addition tool for players to affect the rate of the train

rush. But for 1839 the abstract and infinitely well-funded foreigners didn’t sit well. I want a way to represent the hurdy gurdy jolting of how the Netherlands was tossed about on the technological and political waves of its geographic neighbours. Additionally, the 1843 model seemed as if the game were providing a control knob for only one half of the control system and that it would be inherently more interesting if player controls for both ends were somehow implemented, thus providing some level of tension between the two in influencing the train rush.

The specific thought is for:

- The foreigners to be limited in their train-buying by their capitalisation.

- Players to directly affect the rate at which the foreigners can buy trains by affecting the foreigner’s capitalisation.

- Company operations to affect the train rush rate in the normal manner through their train buying, but also by affecting the foreigner’s capitalisation.

- A lumpy rush/dawdle train-buying pattern by the foreigners which is yet deftermiistic and player-predictable.

- An implicit brake on the system such that if the foreigner’s train buying did rush and suddenly buy many trains, it would then slow down and some provide respite.

Proposal

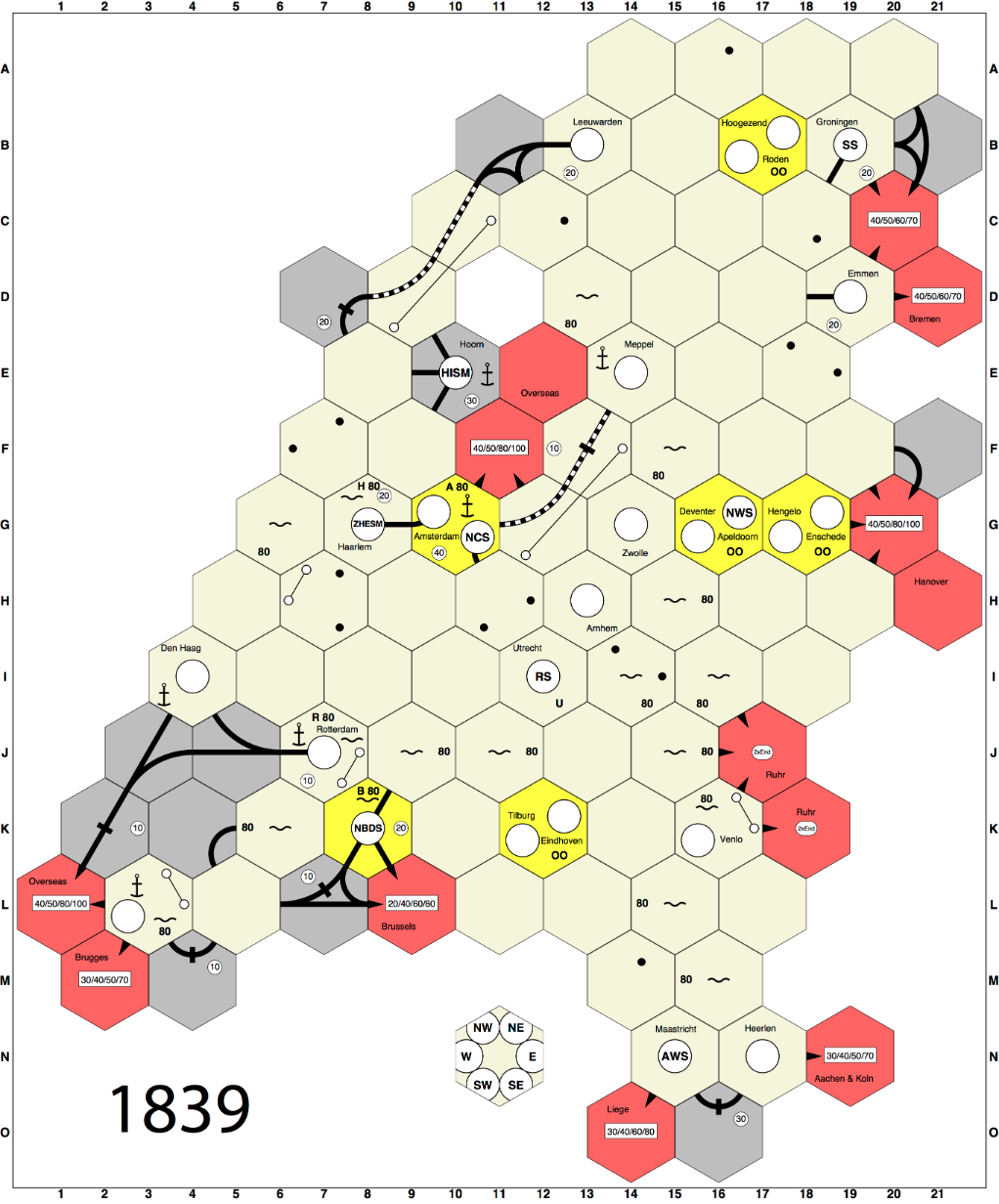

- Each off-board would be a 10-share company that “floated” as soon as a public company ran a train to them.

- The initial stock price of the off-board company would be the highest par price available in the current game-phase.

- The off-boards would effectively be incrementally capitalised companies.

- Public companies would be required to run at least one train to an off-board if possible.

- A thematic addition could be that all of a company’s routes must intersect, ala 1860.

- As public companies operated, the bank would pay 20% of the company’s total revenue to each off-board included in one of their trains’ routes.

- At the end of the Operating Round, after all public companies had operated, the off-board companies would run in descending order of stock price, and would pay dividends, from the bank, to their shareholders based on an assumed revenue of the total amount collected from the bank for public company operations.

- The off-board stock price would then move in the normal way (dividend, no-dividend etc).

- The accumulated revenues and dividends would then be swept to the off-board company’s treasury.

- The off-board company would buy-back any of its shares in the pool

for current market price it could afford.

- If the remaining treasury funds are sufficient, the off-board company would buy as many trains as it could afford from the supply.

- Trains would generally run for a third of their purchase price (ala 1843).

- Off-board shares would not count against certificate limit.

First order effects

The general expectation is that some off-boards would be more popular in the early game, as they are (generally) the highest revenue locations on the board and route development to them could be shared, thus accentuating early revenue generaton. Additionally, the constraint of running at least one train to an off-board would encourage route and revenue generation near the off-boards first, and then moving inland as train lengths grew and the map developed.

The capitalisation of the off-boards should scale fairly directly with company activities. In the early game the off-board shares are severe under-performers and thus unattractive for player investments. However players could trash off-board stock prices, in the process marginally capitalising the off-board for the delta between the purchase price and the re-purchase price, and further reducing the off-board’s capital raising from future share sales.

Conversely, in the later game the off-boards become prime investment opportunities. Public shares are starting to become significant liabilities, and some off-boards may well have 4+ public companies running to them, lifting their average dividends above the average dividend of the public companies. And of course the off-board shares would not count against certificate limit – making them extremely attractive for increasingly flush and potentially paper-tight players.

The flight of capital from the public companies to the off-boards would initially accelerate the train rush due to the increased capitalisation from the share purchases (making public company shares even less attractive), but once the initial burst of trains have been bought, the capitalisation rate of the off-boards should slow due to the loss of the dividends from the purchased shares.

Train buying models

Assuming N operating companies, the off-board capitalisation should

approximate $latex company revenue + dividends = 0.2N + 0.2N = 0.4N$, distributed across the participating off-boards. Assuming each company has 2.5 trains (reasonable after the first tranch), and that trains run for an average of one third their T purchase price, the rate of off-board capitalisation in terms of train purchase cost approximates $latex (0.4 * 2.5)T/3 = T/3$. Or more directly, if 3 companies are operating, each with 2.5 trains, and are each running to the same off-board, then that off-board will raise ~enough capital in each OR to buy one train.

What about a late game scenario of 8 operating companies each with 2 trains, collectively running to all 6 off-boards, 4 of the companies are running to 2 off-boards, 5 companies are running to the Ruhr off-board (as it is the most valuable), and all of the off-board shares have sold out?

First let’s look at the Ruhr’s income (where T is the purchase price of a train): $latex 5 * 0.2 * 2T/3 = 2T/3$ In other words, ignoring escalating train pricing, the Ruhr will be purchasing a train every other Operating Round, and two trains every third Operating Round. Ooof, train rush!

What about the ~three other off-boards with only one such active company? $latex 0.2 * 2T/3) = 0.4T/3$ They’ll be buying one train every seven and a half Operating Rounds.

And the ~three off-boards being run by two companies? $latex 0.4 * 2T/3) = 0.8T/3$ They’ll be buying a train every 3.75 Operating Rounds.

Summing the above: $latex 2T/3 + (3 * 0.4T/3) + (3 * 0.8T/3) = 1.86T$ That’s just a smidge (13.34%) under an average of two trains being bought by the off-boards per Operating Round. But of course train-prices are not constant. The unpopular off-boards are going to lag and buy and lag.

The result should be that that train cost progressions should make the off-board’s purchases bursty. As rusting events progress, the base train-cost will rise faster than revenues and companies will run out of capital and be replacing their trains under the Emergency Train Buying Rules, and thus only running a single train rather than the two trains modeled above. At the crudest level this should not merely halve the train-buying rate of the off-boards to just under one train per Operating Round, but to somewhat less as the unpopular off-boards will tend to chase and miss the ever-rising train prices, thus delaying their purchases.

The actual train buying rate will be the sum of a number of wave functions with each off-board running on its own cycle, decelerating as the train prices rise and accelerating as the companies fill with and run fresh trains. When the trains rush quickly, the off-boards will lose their source of capitalisation and slow their purchases. However the accumulation of capital in their treasuries injects latency into this system, even as the revenues fall due to train rusting events, the marginal off-boards will increment over a purchase price threshold and buy a train. The result, I hope, should be an unstably punctuated equilibrium!